Summary by Ben Simpfendorfer, Asia Pacific Lead, Oliver Wyman Forum, Oliver Wyman

18 April 2024 - Over 134 countries representing 98% of global GDP today are exploring central bank digital currencies (CBDCs), with multiple pilots and experiments helping to drive conviction. But how do we ensure that the tokenised money landscape champions the core tenets of innovation, stability, and financial inclusion?

We gathered prominent participants from both the public and private sector at the Elevandi Insights Forum roundtable to discuss the current and future states of digital money, including the drivers for change, the various actors and their roles, as well as the factors to be considered as digital money scales.

We summarise five key takeaways and action points from the roundtable, which was held under Chatham House Rules.

1. Use case innovation and regulation are key to scaling CDBCs and the digital asset ecosystem

In recent years, the digital asset ecosystem has grown considerably. Numerous CBDCs and other forms of digital money have been launched, and 68 countries are in the more advanced phase of CBDC-development, pilot, or launch. With this as the backdrop, the roundtable raised three key factors needed to further scale CDBCs and the digital asset ecosystem: a) established technology, b) regulation, and c) use cases.

Of the three factors, participants seemed to have high confidence that the technology has been adequately developed over the years, with the industry now shifting away from proof-of-concepts (POCs) to focusing on implementing the technology and systems at scale.

As an enabler to scaling the ecosystem, regulations or guardrails must be developed to anchor the value of digital money and provide adequate consumer protection. Much work remains in this space, with multiple open issues identified, including frameworks around KYC and permissions, privacy of transactions, and harmonizing regulations across jurisdictions.

The roundtable also emphasised the need for further innovation as a key driver for commercial adoption of digital money. Participants emphasised replacing existing financial mechanisms with optimised digital-money based options, as well as developing completely new options that can only be unlocked through digital money and digital ledger technologies (DLT).

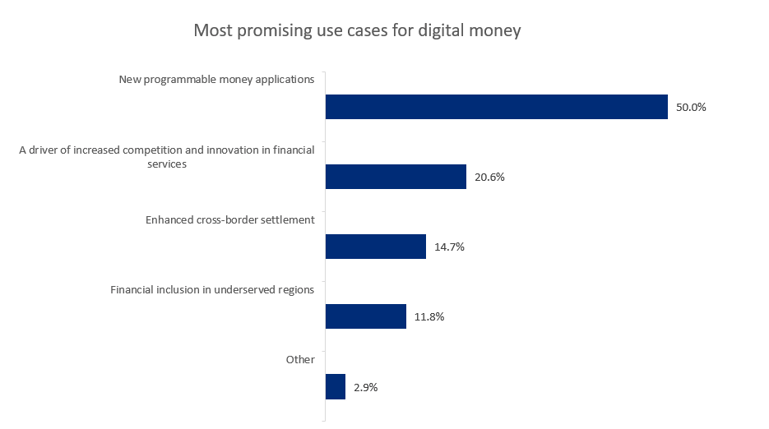

2. Programmable money and smart contracts are receiving significant attention

Figure 1: Poll of audience shows significant attention on programmable money use cases

Emphasis was placed on digital money’s ability to increase cash management efficiencies, reducing both costs and transaction times. By allowing logic from multiple payment systems to be encompassed in one environment, digital money could be multiple times more efficient than existing payment rails that rely on messaging systems to interact.

Furthermore, by allowing for more complex logic to be incorporated, beyond that which is currently possible for traditional treasury management systems, new forms of conditional payments and use cases will be enabled.

3. Interoperability is essential for cross-border payments

Many countries currently face issues with cross-border payments, related to inefficiencies between payment systems and FX exposures. To enable digital money to fulfil its potential and enable faster, more efficient transactions across multiple networks and jurisdictions, interoperability of systems is key – whether this be interoperability of CBDCs or upgraded real-time gross settlement systems. As more blockchain based systems emerge, not only will the interoperability between blockchains be of prime importance, but also that between traditional and blockchain payments systems.

4. Strong confidence in wholesale CBDCs, but questions raised about retail CBDCs

Across the globe, multiple retail and wholesale CBDCs have been rolled out, but with more development focusing on retail CBDCs. Multiple members of the roundtable agreed that wholesale CBDCs have the potential to foster innovation, facilitate more efficient cross-border transactions, and enhance various aspects of the financial system.

However, retail CBDCs were questioned more, from both a use case point of view but also given the fact that retail activities traditionally sit outside of central bank mandates. In particular, issues around transaction privacy, disruption of the existing two-layer banking system and financial integrity were raised as key issues that central banks will have to negotiate.

5. Complementary roles of public sector and private sector

Consensus during the roundtable was that the public sector and private sector will likely play complementary roles in the future digital money ecosystem. Central banks and regulators will safeguard the overall integrity of the financial system, whilst ensuring accessibility and inclusion for all citizens by setting monetary policies. As part of this, CBDCs will act as a stable anchor or reference value for digital money and its transactions.

On the other hand, the private sector can leverage the infrastructure provided by the public sector to innovate diverse payment options. Various forms of tokenised money will allow users significant optionality. In turn, promoting competition, consumer empowerment in the payment ecosystem and contributing to the overall dynamism of the financial ecosystem. As an analogy, the public sector might be considered to be building the ‘highway’ or the foundation and structure for the private sector to drive their various cars, model trucks, motorbikes on it, and serve consumer needs.

The session was moderated by Oliver Wyman’s Ben Simpfendorfer, Asia Pacific Lead of the Oliver Wyman Forum, Oliver Wyman, and Dr Oliver Wuensch, Head of the Swiss Financial Services Practice / Sovereign Finance & Central Banking.

COMMENTS